Market Review Q1 2025 | Market Review Q2 2025 | Market Review Q3 2025 | Market Review Q4 2025

First Quarter 2026

Black is the New Gold Lining in a Cloudy Quarter

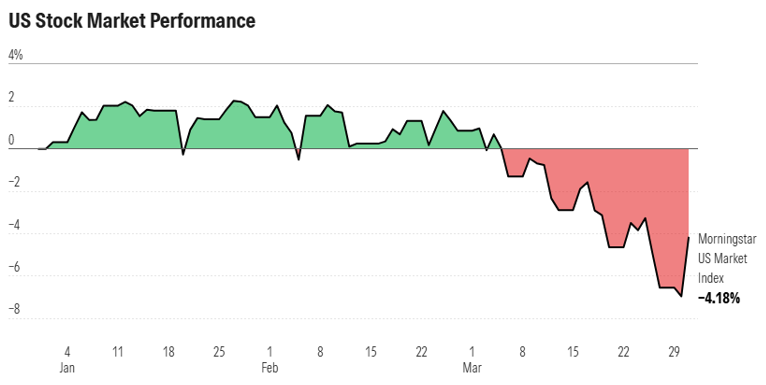

As we entered 2026, market indications pointed to a potential fourth consecutive year of positive stock market results. Early optimism was focused on continued Artificial Intelligence (AI) adoption and expectations of lower interest rates across the yield curve. The Dow Jones Industrial Average reached an all-time high of 51,512.79 on February 10. However, sentiment shifted quickly following the February 28 joint US/Israeli strikes on Iran. Financial markets reacted immediately. Major equity indexes tumbled, while energy prices soared, marking a clear turning point for the quarter.

Equity Commodities: Oil Surges, Gold Volatile

Energy markets experienced significant disruption during the quarter. West Texas Intermediate Crude oil, the U.S. benchmark, climbed roughly 8% in the days following the escalation. The closure of the Strait of Hormuz in March then drove Brent Crude oil, the international benchmark, up 63% in a single month, the largest monthly gain in four decades.

Gold, typically viewed as a hedge against inflation and uncertainty, rose 54% in 2025. In early 2026, it reached a record high of $5,354 an ounce on January 29 before dropping 18.5% to $4,551 at its March low. This pullback was driven by the Fed remaining hawkish, higher Treasury yields, and a stronger dollar. Despite this volatility, gold finished the first quarter with a positive 7.8% return. Analysts generally agree that gold will continue to be perceived as a hedge.

The divergence between oil (often referred to as “black gold”) and gold highlights how different asset classes can respond uniquely to geopolitical events. Should some relatively short resolution be achieved in Iran, we could see prices of gold and oil somewhat revert to previous levels. Importantly, the U.S. economy is less vulnerable to higher oil prices than in the past due to its position as a net exporter of oil.

Source: Morningstar Data as of March 31, 2026. Performance shown in USD.

Equities: Leadership Rotation Emerges

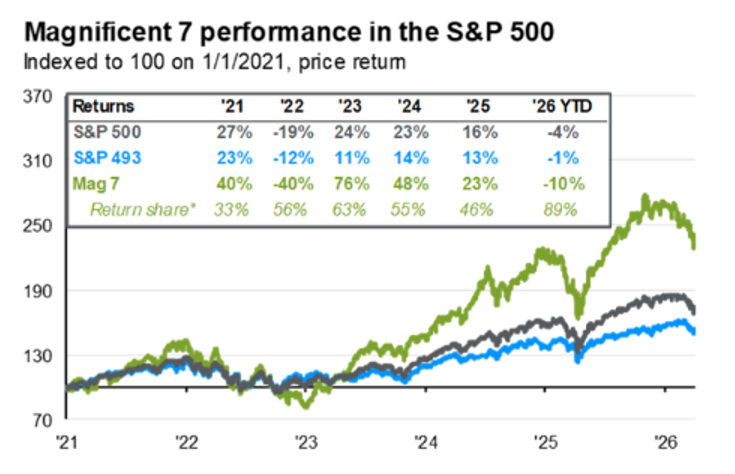

The U.S. Large Cap market, as measured by the S&P 500, was down 4.6% for the quarter, with a notable changing of the guard in leadership away from the largest technology companies. The Magnificent 7 Stocks, known as the Mag 7 and consisting of Amazon, Apple, Facebook, Google, Microsoft, Nvidia, Tesla, had pushed the U.S. equity market to double digit returns in the last 3 calendar years, contributing to a significant percentage of the S&P 500’s performance. The cumulative returns for the Mag 7 over the three-year period was 222%, compared to 52% for the remaining 493 stocks, according to Seeking Alpha. These seven companies continue to represent a significant portion, about 32.5%, of the market. The Mag 7 dropped 10.5% this quarter, while the other 493 companies fell just 1.3%, which accounted for 89% of the S&P 500’s overall decline. Software companies in particular were the most challenged with market stalwart Microsoft falling 23.4% - its worst quarter since 2008.

Source: Bloomberg, FactSet, MSCI, NAREIT, Russell, Standard & Poor's, J.P. Morgan Asset Management

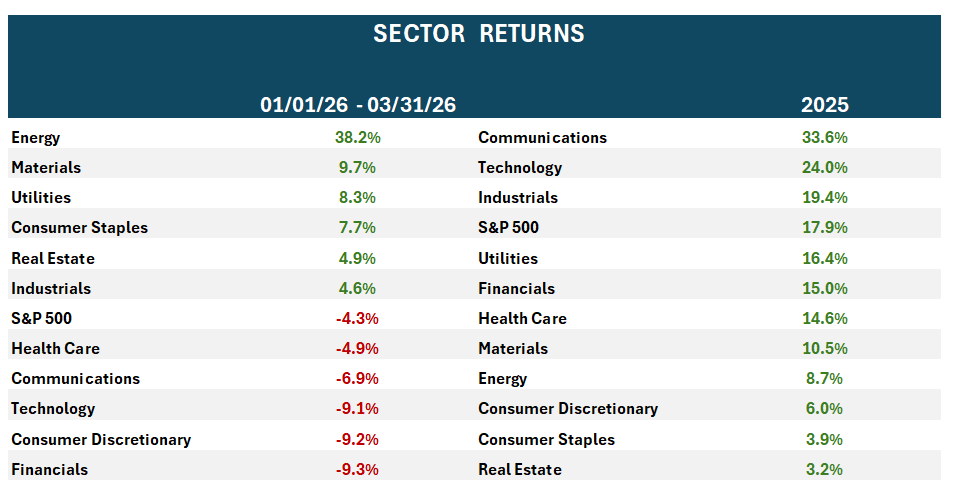

Sector performance also shifted meaningfully. Energy, Consumer Staples, and Materials, which had finished 2025 in the bottom five sectors, led the index for the first quarter of this year, finishing in the top four sectors. Meanwhile, Technology fell from the number two spot in 2025, landing in 9th position at the end of this quarter. Large Cap stocks were also outpaced by small and mid-capitalization stocks, which returned 3.51% (S&P 600 Index) and 2.50% (S&P 400 Index) respectively.

Source: FactSet

In 2025, International Equities significantly outperformed their U.S. counterparts. This trend continued into the first quarter, which provided a bright spot for diversified portfolios. Many regions benefited from the rotation out of technology stocks. A standout performer was the Japanese Topix Index, which returned 3.6% following 2025’s double digit returns. Japan appears poised for continued market strength following February’s elections, which installed a pro-growth, pro-investment government.

Fixed Income: Volatility Returns

The bond market began the year with a rally, given the anticipation of rate cuts by the Federal Reserve and a cooling of some economic data. However, geopolitical developments quickly altered this trajectory. The 10-year Treasury yield dropped to 3.97% in early February, as investors bought bonds in anticipation of rate cuts. The 10-year Treasury closed the quarter with a 4.31% yield, having briefly reached 4.48% towards the end of March.

Investors grew wary of risk and shifted away from Investment Grade Corporate Bonds, which could be vulnerable to energy price shifts. Corporate Bonds, as measured by the Bloomberg US Intermediate Corporate Index finished down 0.15% for the quarter compared to the Bloomberg Intermediate Government/Corporate Index, which was down 0.02%. Emerging Markets Debt also finished in the negative, as investors sought safety in U.S. Treasuries.

The Importance of Diversification

Market volatility is a normal feature of investing. While this quarter’s disruption was driven by geopolitical events, similar periods have occurred throughout market history. We have witnessed both stock and bond market corrections over the course of market cycles due to many different economic factors or events, such as the Financial Crisis in 2007 or Tech Wreck in 1999. This current volatility caught markets off guard, given the prior three years and positive start to the year.

Diversification remains one of the most important tenets of investing, as it serves to dampen volatility in portfolios. As discussed above, small and mid-cap stocks, gold, and international equities all had positive returns in the first quarter. A balanced portfolio, which included all of these asset classes, as well as fixed income, finished the quarter with a positive 1.3% return, underscoring the benefit of diversification, which protects portfolios from unknown events.

Active portfolio management, including periodic rebalancing, also plays an important role. Capturing gains and reallocating across sectors and asset classes can help preserve returns as market leadership evolves.

Outlook

Looking ahead, economic conditions remain relatively stable. The unemployment rate remains steady at 4.3%, and productivity continues to increase through a strong workforce and AI adoption. GDP will be moderate this year, with a modest boost from increased tax refunds in the second quarter. Should oil prices recede, it is anticipated that one interest rate cut will be implemented. As of April 2, FactSet reported the estimated growth rate for S&P 500 earnings to be 13.2% year-over –year, which could mark the 6th straight quarter of double-digit growth for U.S. earnings.

While uncertainty persists, these factors could bode well for the markets, and portfolios, to weather this current climate. At Cape Cod 5, we remain focused on guiding clients through choppy waters, as well as calm seas, with a disciplined, long-term approach to investing.

Kimberly Williams

Senior Investment Officer

On behalf of the Cape Cod 5 Trust and Asset Management Investment Team

Rachael Aiken, CFP®, Chief Wealth Management Services Officer

Michael S. Kiceluk, CFA, Chief Investment Officer

Brad C. Francis, CFA, Director of Research

Nancy Taylor, CFA, CAIA®, Senior Investment Officer

Jonathan J. Kelly, CFP®, CPA, Senior Investment Officer, Manager, Financial Planning

Craig J. Oliveira, CFA, Senior Investment Officer

Robert D. Umbro, Senior Investment Officer

Benjamin M. Wigren, Senior Investment Officer

Jack Dailey, Investment Analyst

Alecia N. Wright, Investment Analyst

These facts and opinions are provided by the Cape Cod 5 Trust and Asset Management Department. The information presented has been compiled from sources believed to be reliable and accurate, but we do not warrant its accuracy or completeness and will not be liable for any loss or damage caused by reliance thereon. Investments are NOT A DEPOSIT, NOT FDIC INSURED, NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY, NOT GUARANTEED BY THE FINANCIAL INSTITUTION AND MAY GO DOWN IN VALUE.