Market Review Q1 2023 | Market Review Q2 2023

Third Quarter 2023: Sideways

“I don’t want to be sideways. I just want to be going forward.”

– Miles Raymond in the movie Sideways

The lion’s share of the third quarter market activity could be aptly described as ‘sideways’ by many counts, but the market loves to remind us that it only needs a couple of days to introduce a new theme and provoke a response accordingly – and it did just that late in Q3. The new theme could be characterized as ”worry” – in this case, increased worry about a recession coming sooner, rather than later or not at all. The domino that started the quarter-closing, two-week selloff in equity markets was the sudden spike in longer-term interest rates and what these rate increases might mean for short-term economic activity.

The third quarter started with the S&P 500 at 4,450 and the 3-year Treasury yielding 4.56% and remained relatively consistent through September 15, when the S&P was at 4,450 and the 3-year Treasury was yielding 4.72%. Then, a switch flipped. Volatility increased and prices changed quickly. The last two weeks of September saw a small echo of the market moves of 2022 – higher interest rates, lower equity prices, and higher energy prices. The S&P dropped 3.6% to 4,290, and interest rates spiked higher, with the 3-year Treasury rate climbing to 4.88% – an auspicious end to the quarter that leaves investors wondering how the year will close out.

What will bring us to a better place, a place filled with hope for current investors? For those with investment portfolios, a place of hope means a “soft landing” – inflation comes down meaningfully over the next year, the unemployment rate rises (but not too much), and economic growth slows but doesn’t reverse. Both stock and bond markets would reward this scenario, but before we begin that journey, it’s important to remember how far we’ve come in 2023. At the start of the year investor sentiment was incredibly bearish – the Consumer Sentiment Index sat below 60, near 50-year lows. The S&P 500 sat at about 3,800 and most market prognosticators were debating how much lower it would go. There was some light on the horizon, and it was led by the ever-resilient U.S. consumer and the sense that the large inflation wave of 2022 had peaked and was coming back to earth.

Though we have made some great progress this year, the third quarter has also reminded us that, besides our longtime foe inflation, higher oil prices, labor strikes, and a possibly more troubled consumer are new factors that could prove problematic.

Inflation: Declining, but not fast enough

Inflation has been the dominant factor influencing both bond and stock markets for almost two years. During the third quarter, it has become apparent that this will remain the case until the Fed’s target of 2.0% is reached.

The start of the quarter showed some promise of getting closer to the Fed’s target, but also some signs of stickiness that had markets slightly anxious. The headline Consumer Price Index (CPI) came in at 3.1% in June, which contributed to continued optimism in the equity markets. However, readings for July and August of 3.3% and 3.7%, respectively, prove that there is still some distance to travel.

The Federal Reserve focuses on the core rate, which excludes the volatile food and energy components, which continues to trend lower – the core rate at the end of Q2 stood at 4.9% while the latest reading for August showed 4.4%. Shelter costs have noticeably cooled since last year as have used car prices, which have now seen price declines for three straight months.

One factor that we will be watching, and may represent a pothole in our road, is energy prices. Oil had dropped from last year’s highs of over $100/barrel, trading below $70 early this summer, and has since regained higher price momentum. Oil ended Q3 trading at about $90 and this has led to overall higher non-core inflation and a headwind on equity markets.

Interest Rates and the Federal Reserve: Higher and Longer

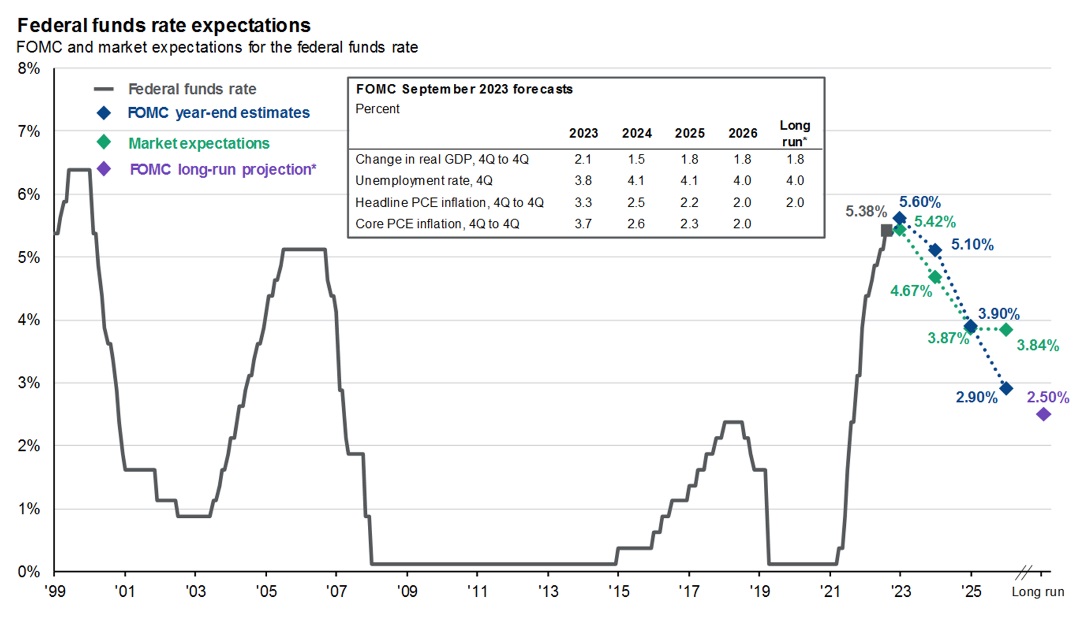

The Fed’s latest interest rate decision came at the end of September and their decision was not a surprise – no change. This followed a 0.25% hike at the July meeting that brought the overnight borrowing rate to a guided range of 5.25% – 5.50%. What was unexpected and caused some turbulence for both the stock and bond markets, was the guidance going forward. Chairman Powell and the other Fed governors believe they will have to keep rates higher for longer and may have to hike rates once more before year end.

The bond market has been continuing its disbelief in the Federal Reserve’s resolve to hold rates higher and they have continued to be wrong. Once again, the estimates for the Fed Funds Rate have risen, with 2024 now at 5.1% and 2025 at 3.9%. Both projections have risen by about 0.50% over the last three months.1

Source: Bloomberg, FactSet, Federal Reserve, J.P. Morgan Asset Management

In the face of this more hawkish guidance, the Fed’s Summary of Economic Projections sees a path to a “soft landing”. They updated their June forecast of real 2023 GDP growth to 2.1% from the earlier June guidance of 1.0%. Furthermore, they see the 2024 unemployment rate averaging 4.1%, down from June’s outlook of 4.5%. These optimistic forecasts may be hard to achieve in a longer-term, higher interest rate environment.

Economy – Not Crying Wolf, but Recession?

2023 might go down as the year where everyone waited for a recession that never came. And there were good reasons why many economists were predicting a recession – the yield curve has now been inverted for 15 straight months, the Manufacturing Purchasing Managers Index (PMI) remains in a prolonged state of contraction, and the Conference Board’s Leading Economic Index continues to signal a recession, as it has since mid-2022. So why hasn’t it arrived?

As a reminder, a recession is usually defined as two consecutive quarters of negative gross domestic product (GDP). GDP measures the total value of the output of goods and services in the economy and, despite much higher interest rates which usually act as resistance to economic expansion, U.S. GDP continues to remain relatively strong at a 2.1% annual growth rate.

There is little doubt that what has kept the economy humming along – and what may eventually prove its undoing – is the U.S. consumer. Consumer spending has remained strong through this period of rising interest rates, rising at a real rate of 1.3% over the six months ending August 31.2

Headwinds, however, are increasing for the U.S. consumer. Mortgage rates below 3.0% are a thing of the past, with the average 30-year mortgage rate now at 7.5%.3 The freeze on student loans has expired and payments on loans are set to begin again in October. Finally, government stimulus payments during COVID that were placed in savings have been drawn down and the usual healthy appetite for holiday spending might be curtailed this year.

One bright spot helping the U.S. consumer is the still low rate of unemployment. The heralded “Great Resignation” that began during COVID has been rewound and the percentage of the important 25-54 age group working has hit twenty-year highs at 83.5%.4 The strength of the labor market works as a double-edged sword – healthy wages fuel consumer spending which drives economic growth, but this competition for labor leads to stronger wage increases and further, perhaps persistent, inflation. The current labor strikes in the auto industry add support for this view and how they are resolved, and on what terms, will have a big impact on whether we will have that soft landing.

Markets – Following the Playbook (for Now)

The stock market started the third quarter by continuing the momentum it had established during the first half of the year – July saw the S&P 500 gain 3.2%, taking the index up just over 20.0% for 2023. The standout index of the year had been the heavily technology-weighted NASDAQ, which remained strong, rising 4.0% in July registering year-to-date gains of 38.0%. Just when everyone was starting to enjoy this surprising summer strength, the market peaked. From the S&P high of 4,600 as of July 31, the market gains began to slowly erode, culminating in a steeper selloff in the last two weeks of September.

The third quarter saw declines in all sub-asset classes of the equity market, with small caps lagging the most, down 5.0% for the quarter. International markets also pulled back, although emerging markets outperformed the more developed regions. Even the 2023-leading NASDAQ pulled back 4.0% in the quarter to finish up 27.0% year-to-date.

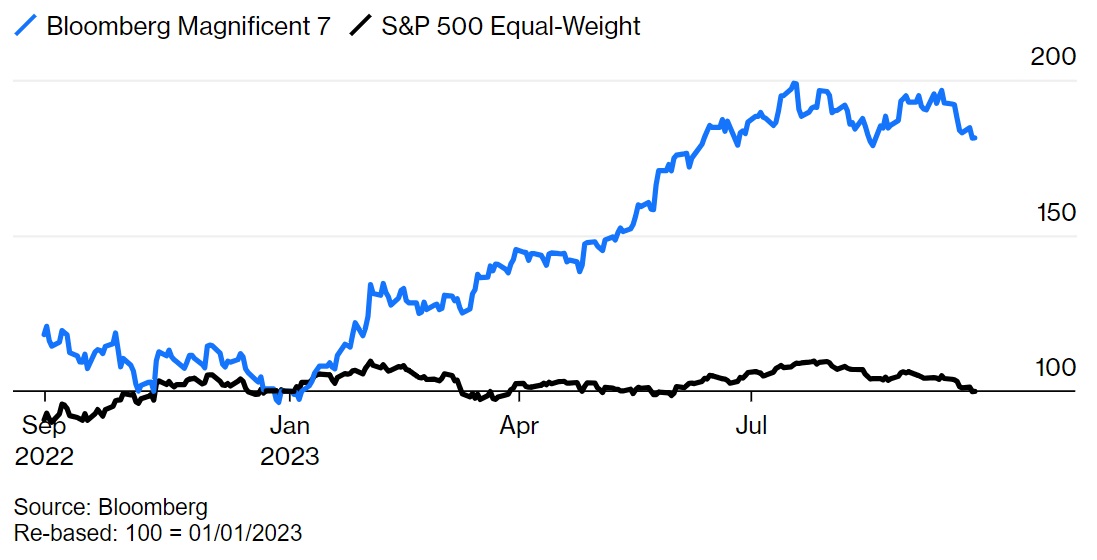

This year to date has been highly unusual in that almost all the stock market gains can be attributed to the performance of the “Magnificent Seven”: Apple, Microsoft, Nvidia, Amazon, Meta, Tesla and Alphabet. These seven stocks are up about 80.0%, while the other 493 stocks in the S&P have treaded water, barely showing any average positive return. A well-diversified investor with little exposure to these tech giants might have negative returns for the year. The graph below aptly illustrates the outperformance of the Magnificent Seven.

The big question now is how much longer this outperformance can continue, and indeed, September saw these stocks start to pull back. Fueled by the increased hype over AI, investor sentiment helped power their returns, and for now the market is in wait-and-see mode. Will we see AI products for consumers come soon, and will the revenues from these products meet expectations? Will we be closely watching Microsoft’s launch of “Copilot”, an AI assistant, as this is coming to the Office 365 suite of products now and will be available for all business consumers this fall. Copilot may prove a catalyst for further AI enthusiasm or a reason for investors to fade the hype.

Looking Ahead to 2024

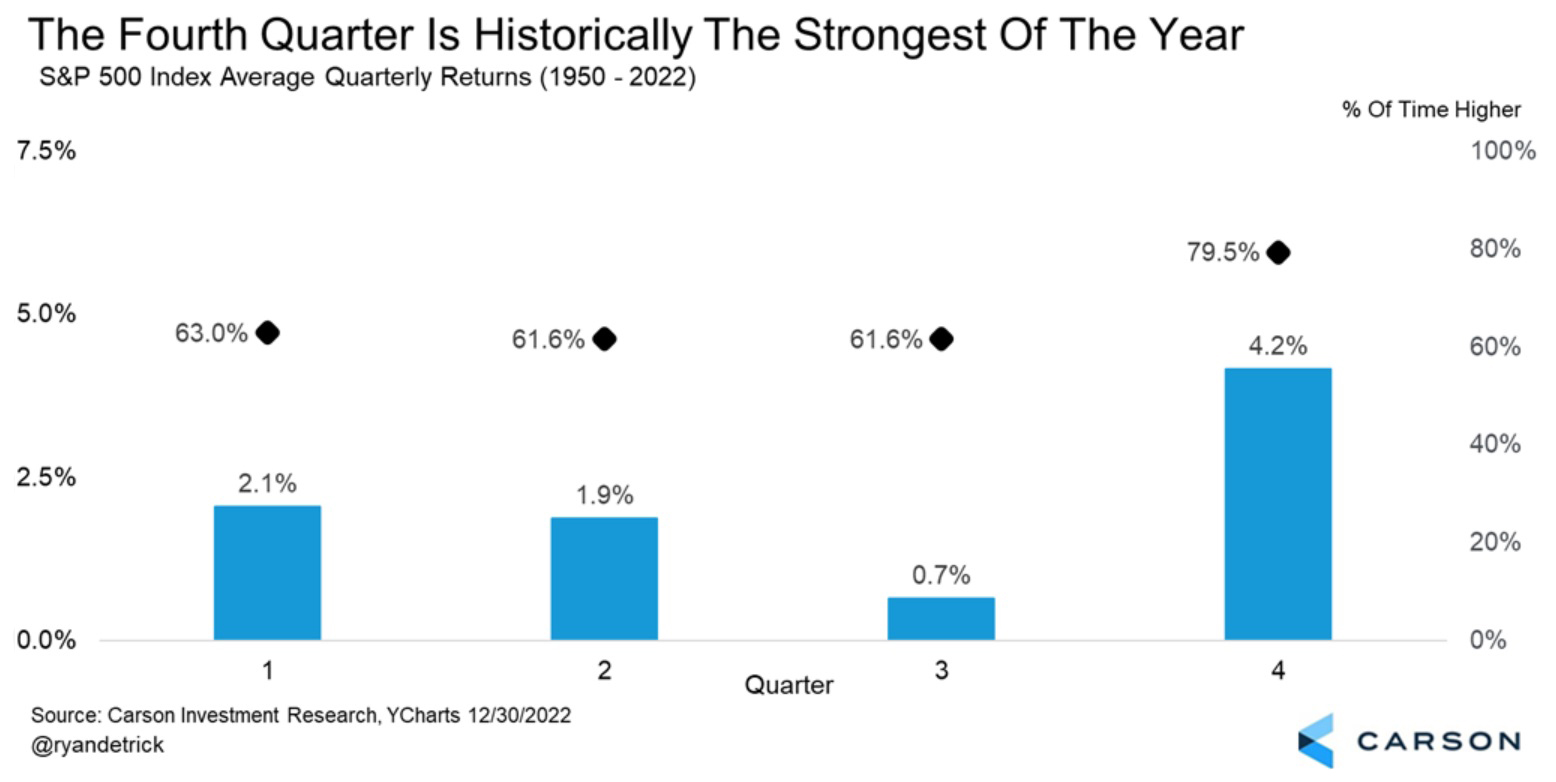

As we enter October, a notoriously volatile month for markets, one might have doubts about the market's progress in the near future, but a strong argument favoring a positive quarter could be made based on how well markets have traditionally done the last quarter of the year, as shown in the following chart.

Not only are we entering the strongest time of the year for markets, but this momentum usually carries forward through January.

These strong market trends will be tested by a host of factors – rising oil prices, labor strikes, high interest rates, geopolitical conflicts, and government shutdowns. The key remains inflation, the Fed’s continuing response to it, and whether the resolute U.S. consumer remains strong or is forced to curtail their spending.

We value your continued faith in Cape Cod 5 as your trusted financial advisor and encourage you to contact your investment professional if you have questions about how this information impacts your specific portfolio.

Jonathan J. Kelly

Senior Investment Officer

On behalf of the Cape Cod 5 Trust and Asset Management Investment Team

Michael S. Kiceluk, CFA®, Chief Investment Officer

Brad C. Francis, CFA®, Director of Research

Rachael Aiken, CFP®, Senior Investment Officer

Jonathan J. Kelly, CFP®, CPA, Senior Investment Officer

Nancy Taylor, CFA®, CAIA®, Senior Investment Officer

Robert D. Umbro, Senior Investment Officer

Benjamin M. Wigren, Senior Investment Officer

Kimberly K. Williams, Senior Wealth Management Officer

Craig J. Oliveira, Investment Officer

Jack Dailey, Investment Analyst

Alecia N. Wright, Investment Analyst

1 “The Federal Reserve’s Dotted Line on Interest Rates,” Wall Street Journal, 09/20/2023

2 “Guide to the Markets,” J.P. Morgan, as of 09/20/2023, page 19

3 "30-Year Fixed Rate Mortgage Average in the United States," FRED Economic Data, St. Louis Fed ,10/05/2023

4 “Labor Participation Rate – 25-54," FRED Economic Data, St. Louis Fed, 10/05/2023

These facts and opinions are provided by the Cape Cod 5 Trust and Asset Management Department. The information presented has been compiled from sources believed to be reliable and accurate, but we do not warrant its accuracy or completeness and will not be liable for any loss or damage caused by reliance thereon. Investments are NOT A DEPOSIT, NOT FDIC INSURED, NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY, NOT GUARANTEED BY THE FINANCIAL INSTITUTION AND MAY GO DOWN IN VALUE.