Market Review Q1 2023 | Market Review Q2 2023 | Market Review Q3 2023

Fourth Quarter 2023

Year-End Economic Review: Cautiously Optimistic

2023 gave investors myriad reasons to rejoice after the abysmal performance of both equity and bond markets in 2022. Positive market performance in 2023 not only provided relief, but also stellar performance in sectors such as technology, communications services and consumer discretionary that houses the “Magnificent Seven” stocks. GDP growth surprised to the upside, marked by a significant uptick in 3Q at a 4.9% seasonally adjusted annual rate, defying the Fed’s attempt to cool economic growth. Although consumer spending remained resilient, there exists a conundrum of lackluster confidence and expectations levels despite the Fed’s headway on tamping down inflation, continued strength in the jobs market and the equity market recovery. This dynamic could reflect caution on what the next shoe to drop might be. Geopolitical uncertainty abounds with the war in Ukraine dragging on and now the war in Gaza which risks expanding into a larger regional conflict. Potential expanded U.S. involvement in these wars adds to the already heavy U.S. financial and weapons support. These risks and the upcoming polarized U.S. presidential election are certainly top of mind for many.

The Coveted Soft Landing

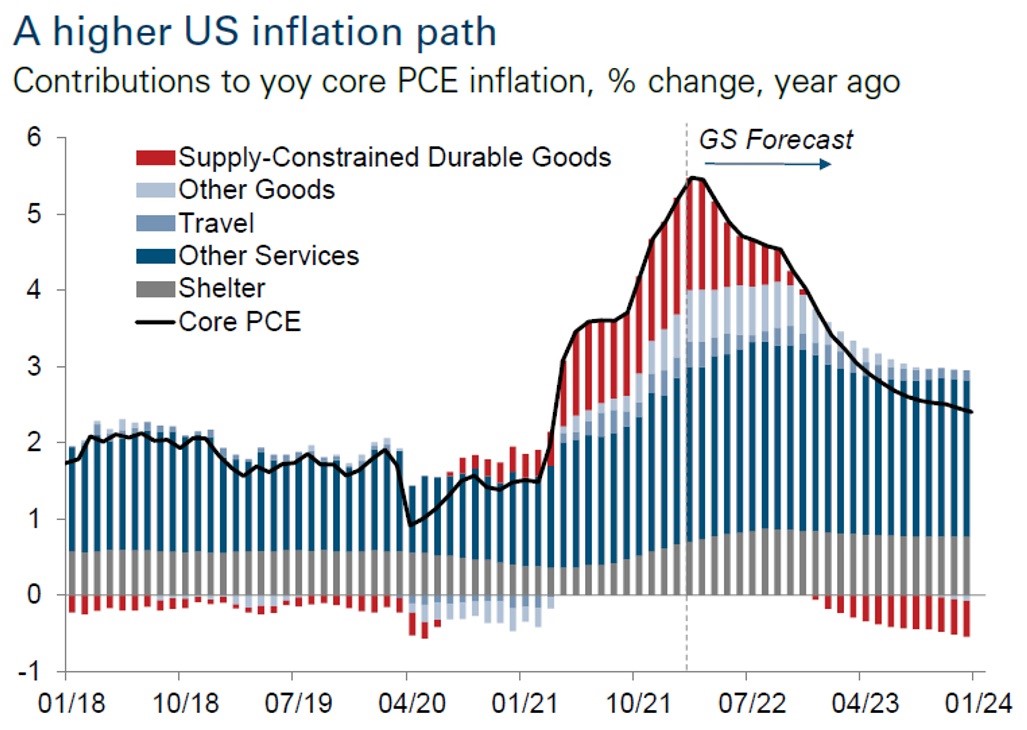

Although it seems too good to be true, the Federal Reserve Board’s objective over the last two years to tame inflation without triggering a recession, otherwise known as a “soft landing,” may come to fruition. The imbalances in the supply chain largely caused by repercussions of the pandemic mostly resolved themselves last year, helping to ease many of the pressures which caused inflation to spike in 2021 through early 2023. On the demand side, the discontinuation of federal COVID-19 benefits to some individuals and businesses likely impacted spending. Supply and demand appear more balanced now than they have been in the last 3 years. As a result, inflation rates came down markedly in 2023, yet are not at the Fed’s 2.00% year-over-year goal. The Core PCE (Personal Consumption Expenditures, excluding food and energy), a favored metric used by the Fed to gauge inflation’s impact on consumers, declined to 3.2% in November, falling more than expected.

Source: Goldman Sachs GIR

With inflation rates showing consistent declines, the Federal Reserve’s rate hiking cycle has been on pause since July, allowing the delayed impacts of monetary tightening to work their way through the economy. With a Fed Funds Rate in the range of 5.25%-5.50%, consumer lending rates increased with the most prominent impact in mortgage rates, which neared 8.0% in October. Home sales plummeted to new lows in the quarter from the combination of these higher lending rates and historically low inventory.

The Fed’s other mandate, to promote full employment, has remained in a healthy position with the unemployment rate remaining below 4.0% since December 2021 and stronger than expected new job growth. In 2023, the U.S. saw the creation of almost 2.7 million new jobs and maintained consistent growth in wages at over 4.0% year over year. The unexpected strength in the jobs market has left the Fed hawkish in their policy as demonstrated by the minutes from their last policy meeting, spelling out that additional rate hikes are not off the table and rates may remain higher for longer.

Equity Markets

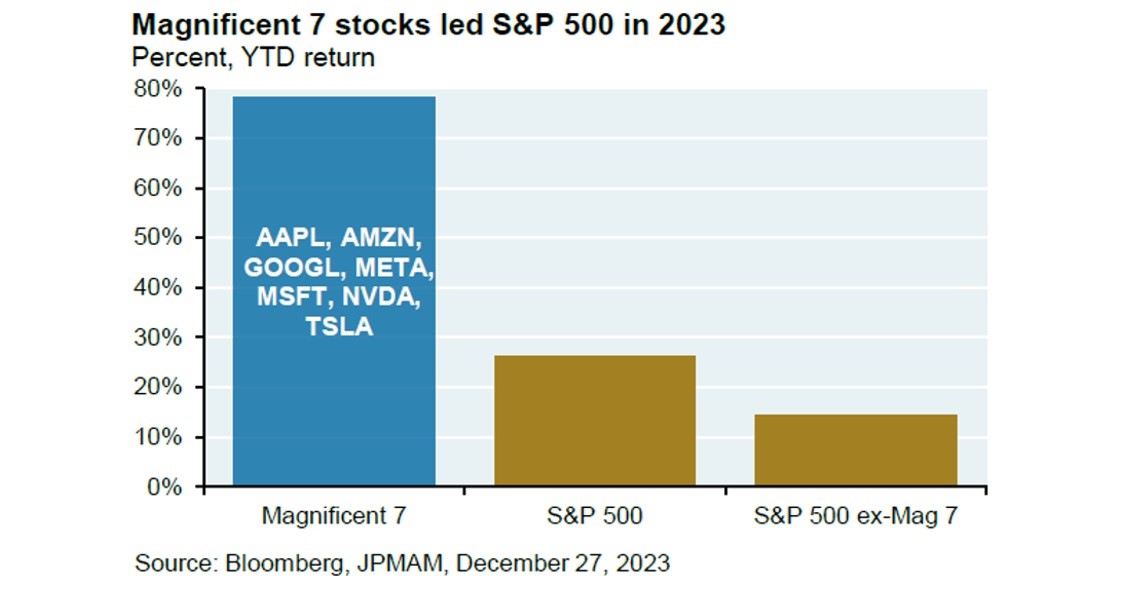

U.S. and developed markets experienced significantly better returns in 2023 than the previous year, with the S&P 500 Index finishing the year at 4,770, just shy of its all-time high of 4,796 on January 3, 2022. The Nasdaq Index, which has a larger concentration in technology companies, ended the year at 15,011 and remains 6.5% below the high it reached on November 19, 2021, which was 16,057. The equity headline story of the year was that of the “Magnificent Seven”: Tesla, Apple, Alphabet, Nvidia, Microsoft, Amazon and Meta. From a market capitalization perspective, these companies now dominate both the S&P 500 and the Nasdaq 100. The “Magnificent Seven” represents more than 25.0% of the S&P 500 and more than 50.0% of the Nasdaq 100. Their ‘magnificent’ performance in 2023 accounted for the bulk of these indices’ positive performance as the demand for technology solutions, hardware and software continue to grow in the rapidly changing technology landscape.

Source: J.P. Morgan

While this sugar high feels good, it also invites concentration risk into index performance and individuals’ portfolios. Some investors may be concerned that they missed the rally due to an underweight position if holding individual securities. However, concentration risk can impact long-term portfolio performance in many ways. Owning a large concentration in one, or just a few stocks, exposes an investor to increased company specific risk. This is the risk that if there is a negative development with that company or its sector, an investor can experience substantial losses. Also, a large concentration in a high performing stock in a taxable account creates liquidity risk as it is often harder to diversify and reduce concentration when you are faced with a high level of capital gains.

As we enter 2024, the prospect for equity returns based on forecasted corporate earnings growth remains positive barring a recession or black swan event. The consumer continues to buy goods and services, which should propel most businesses in the coming months. Additionally, if economic data supports the notion that the Fed will move to an easing of monetary policy, then we expect the housing market to see a rebound as pent-up demand from buyers may be met with new housing stock and an increase in existing homes for sale.

Source: Data from Morningstar Direct

Fixed Income

The long-awaited pivot

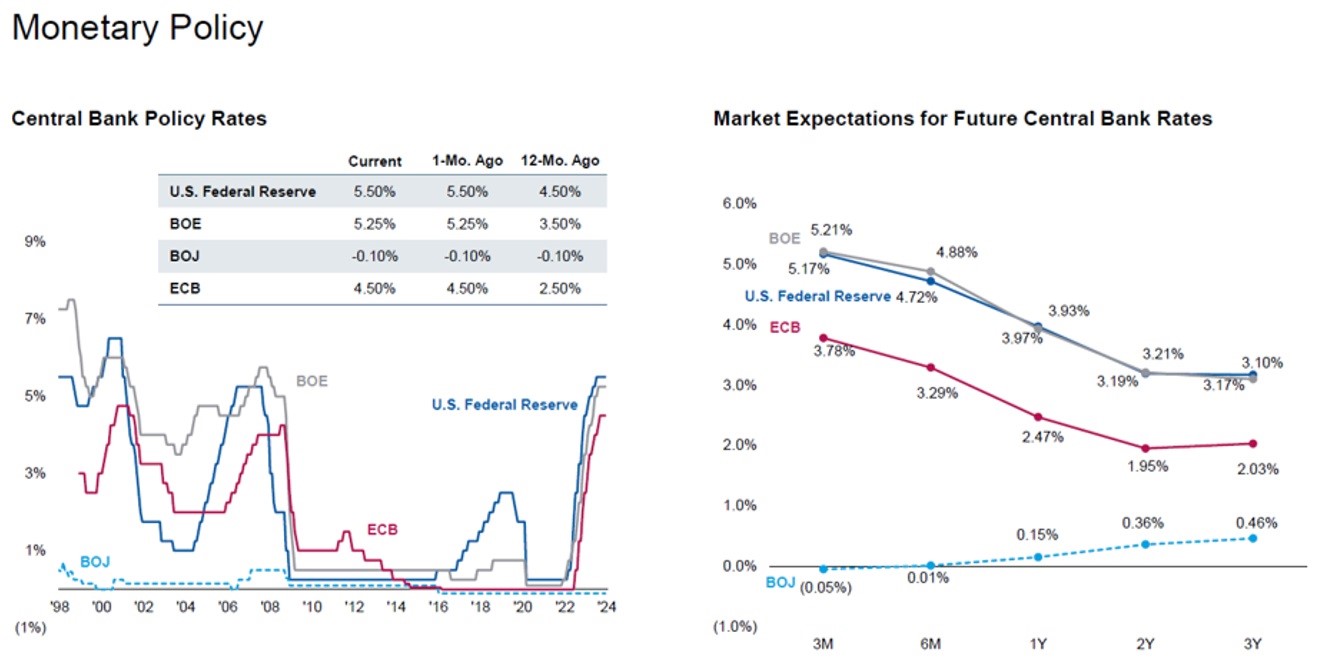

Fixed income markets finally felt relief at the end of the fourth quarter as easing inflation data and a somewhat softer employment picture shifted the tone of the Fed at their last meeting of 2023. With the Fed pivoting to a less hawkish stance, the bond market rallied in the last few weeks of 2023, marked by the 10-year Treasury moving off its recent high of nearly 5.00% in mid-October to end the year at 3.87% on December 29, 2023. Credit spreads narrowed, which indicate a positive outlook on the economy, further contributing to the bond rally. While the Fed remains steadfast in its consideration of additional hikes to the Fed Funds Rate to counter any potential uptick in inflation, the Fed’s dot plot (Fed policymakers' estimates for interest rates at the end of the next several years) is pricing in three 25 bp cuts in 2024, potentially bringing the target rate down a total of 75 bps to a range of 4.50%-4.75%. In contrast, the market remains more optimistic that the Fed has concluded its hiking cycle and will lower rates at a faster clip this year. Currently, the market is pricing in a total of six 25 bp cuts for 2024, for a total reduction of 1.50%. A Fed on hold or shift to easing monetary conditions is good news for the bond market. International developed markets also stand to benefit from easing inflation rates and subsequent changes to monetary policy. As seen in the chart below, the Fed, the ECB and BOE responded to the global inflation spike by raising rates and are expected to begin loosening their monetary policy this year as inflation eases.

Source: Bloomberg, Factset as of 12/31/23. Data provided is for informational use only. See end of report for important additional information. Forecasts/estimates are based on current market conditions, subject to change, and may not necessarily come to pass.

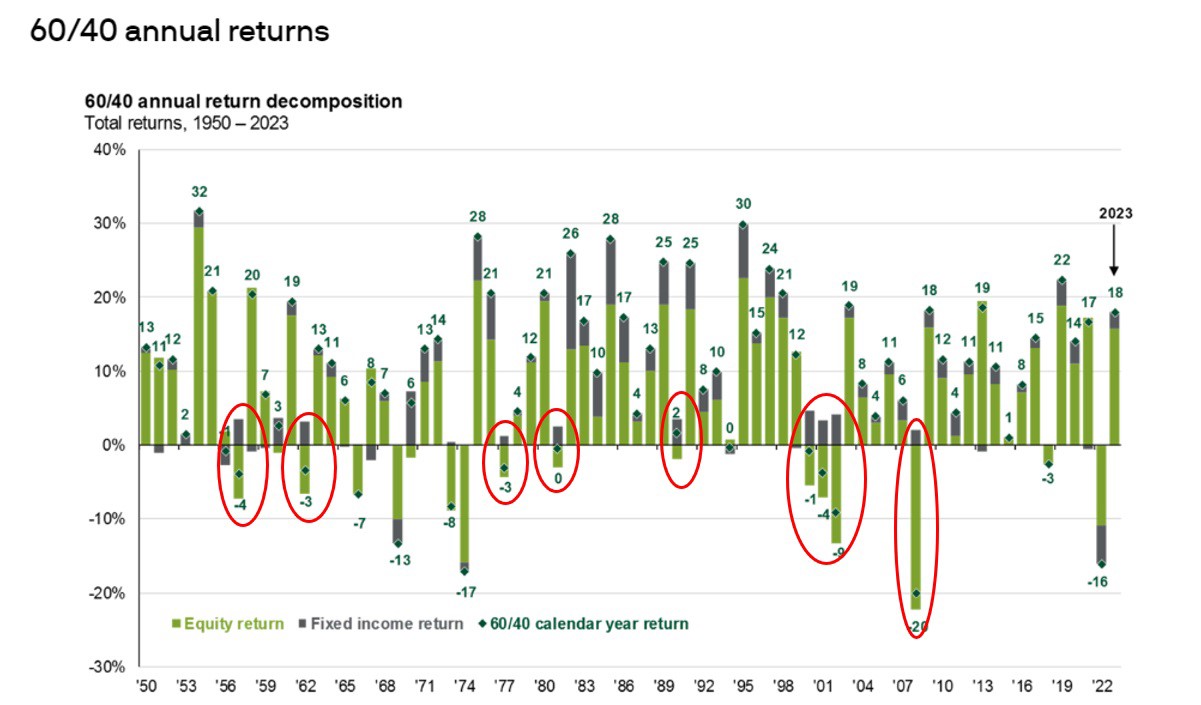

The poor performance of the bond market in 2022, coupled with the negative equity market performance, called into question the merits of the traditional 60/40 portfolio. We believe the traditional relationship of bonds and stocks will revert to their norm (see chart below). We expect bonds to maintain their historic place of value in any diversified portfolio, serving as a ballast in economic downturns and a competitive source of income now that interest rates have moved off the lows of the last several years. As depicted in the chart below and called out in the circled time periods, you can see that usually in times of negative equity returns, bond market performance has been positive with very few exceptions.

Source: Guide to the Markets | J.P. Morgan Asset Management (jpmorgan.com)

For bond investors, 2024 appears to have the right ingredients for continued better yields than we have seen over the past 15 years due to higher coupon income and the potential for capital appreciation if rates decline from the recent highs. In 2023, high yields in money market funds kept many investors heavy in cash as a safe-haven due to the benefit of rising rates and fears of an impending recession that never came to fruition. We anticipate investors deploying excess cash into longer-term bonds and the equity markets as more consensus gathers around expected Fed rate cuts. In 2024, we anticipate bond rates in the 4.0+% range with positive real rates (after discounting for inflation), giving investors the opportunity to benefit from their bond allocations over the long-term.

Alternatives

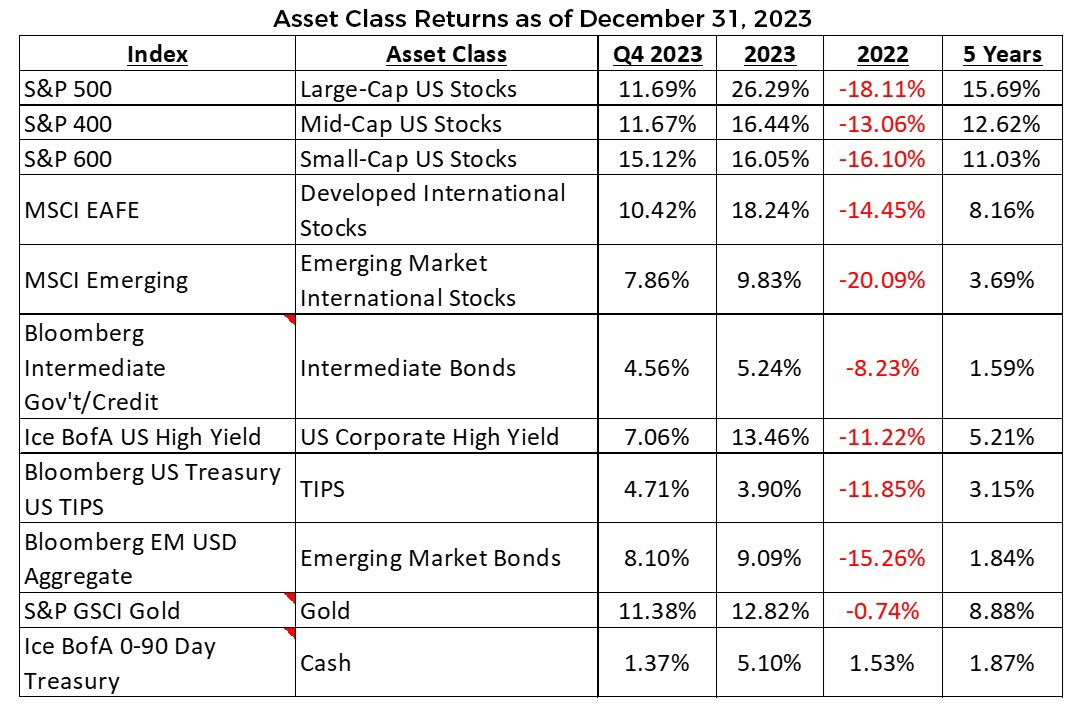

Our focus in the alternatives space continues to be precious metals which serve as a hedge against inflation and economic uncertainty. Last year, gold returned 12.8%, besting the bond market, REITs, emerging markets and cash.

Conclusion

Navigating the markets in 2024 will present many of the same challenges and opportunities we saw last year, however there are three areas to which we will be paying close attention. First, monetary policy of the Federal Reserve Board will dictate much of the mood in the markets and affect both consumer and business credit availability and debt delinquency rates. Geopolitical risks may also resonate through the markets should the tensions escalate, or hopefully, find resolution. Lastly, the results of the 2024 U.S. presidential election will influence future tax policy and government expenditures, and thus their impact on the general economy.

As can be seen from the two years of stark contrast in equity and bond market performance in 2022 and 2023, adherence to an asset allocation plan based on your personal circumstances and risk tolerance is vital. A market downturn can be unnerving, as can losing focus on your goals and watching the market rebound if you sit on the sidelines. At Cape Cod 5, as your trusted financial partner, we seek to help you maintain focus on your long-term objectives during all market cycles and support any adjustment needed to your positioning as your personal circumstances evolve.

Best wishes for a Happy and Healthy New Year. Thank you, as always, for the trust you place in Cape Cod 5.

Nancy Taylor, CFA®, CAIA®

Senior Investment Officer

On behalf of the Cape Cod 5 Trust and Asset Management Investment Team

Michael S. Kiceluk, CFA®, Chief Investment Officer

Brad C. Francis, CFA®, Director of Research

Rachael Aiken, CFP®, Senior Investment Officer

Jonathan J. Kelly, CFP®, CPA, Senior Investment Officer

Nancy Taylor, CFA®, CAIA®, Senior Investment Officer

Robert D. Umbro, Senior Investment Officer

Benjamin M. Wigren, Senior Investment Officer

Kimberly K. Williams, Senior Investment Officer

Craig J. Oliveira, Investment Officer

Jack Dailey, Investment Analyst

Alecia N. Wright, Investment Analyst

These facts and opinions are provided by the Cape Cod 5 Trust and Asset Management Department. The information presented has been compiled from sources believed to be reliable and accurate, but we do not warrant its accuracy or completeness and will not be liable for any loss or damage caused by reliance thereon. Investments are NOT A DEPOSIT, NOT FDIC INSURED, NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY, NOT GUARANTEED BY THE FINANCIAL INSTITUTION AND MAY GO DOWN IN VALUE.