Market Review Q2 2022 | Market Review Q1 2022 | Market Review Q4 2021 | Market Review Q3 2021

Market Review Q2 2021 | Market Review Q1 2021

Market Review

Navigating the Crosscurrents of the Market

The third quarter of 2022 started off with great promise. The S&P 500 stock index ascended from the June lows to a high of 4,320 in mid-August, a climb of over 17%. The 2-year Treasury, a good bellwether of the Federal Reserve’s future interest rate hikes, stabilized around 3% and investors began to grow more confident. In mid-August, the big question asked was whether the current bear market had been slayed or if it was merely a typical “bear market rally”: a sharp run-up in stocks that would give renewed hope to stock market investors only to end in eventual lower prices. The answer came suddenly, ignited by Federal Reserve Chair Jerome Powell’s comments at The Jackson Hole conference on August 26 that the Fed’s interest rate moves will “bring some pain to households and businesses.”1 Equity markets turned sharply negative. The bear had returned.

From the day of Powell’s comments until the close of the quarter, the S&P declined 15% and the 2-year Treasury climbed to 4.2%. The relative calm of mid-summer revealed itself to be a mirage, as markets around the world reacted to a renewed push by central banks to get inflation under control by any means necessary. Dislocation in financial markets continued around the world, most notably demonstrated by the rapid rise in the dollar. In the last year, the dollar climbed 16% against the Euro, 24% against the Japanese Yen, and 18% against the British pound.

Outside of the ongoing crisis in Ukraine, inflation and central bankers’ interest rate policies are most responsible for the turmoil we have seen in world markets in 2022. Just as higher inflation has led to the rout in equity and bond markets in 2022, the path to stability and increased economic growth will come by defeating this persistent foe.

Inflation

Over the summer it became clear that inflation would not be tamed so easily. The Consumer Price Index (CPI) climb of 9.1% year over year for the month of June was the highest since November 19812 and, though it has backed off slightly since that peak, it remains stubbornly high. It is important to remember that inflation is not only a U.S. problem, and has manifested in other large economies throughout the world. Consumers and businesses worldwide have not experienced inflation in many years and the impact of persistent inflation on the economy is key to why the Federal Reserve is going to such lengths to get inflationary price increases under control.

Inflation, at its core, erodes the value of your money. If inflation is running at 8%, it means, on average, the cost of everything purchased – whether it be groceries, fuel, or rent – has increased by 8%. As we saw earlier this year with gas prices, some goods can increase far more than this, putting inordinate pressure on many households as their paychecks cover less. For companies, inflation can hurt in a myriad of ways. Labor is one of the biggest cost-drivers for corporations and when workers demand higher wages to keep up with rising prices, operating margins are impacted, resulting in declining earnings. Moreover, with rising input costs, business leaders are reluctant to invest in long-term capital projects, as their future costs and benefits become more difficult to predict. This slowing of investment acts as a drag on economic growth and, as the economy stalls, people experience an overall decline in their standard of living.

Interest Rates

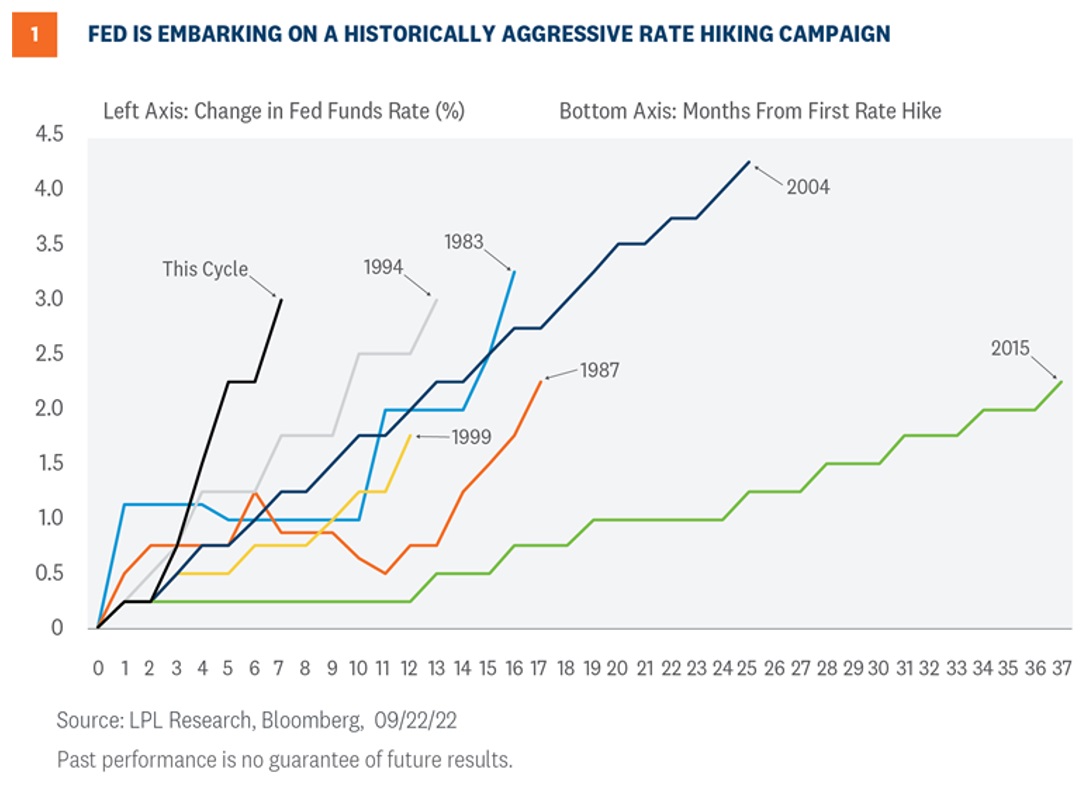

While inflation is the monster that must eventually be slayed, it is the weapon used to slay this monster that does the most damage to bond and equity markets. That weapon is interest rates. The one rate that the Federal Reserve directly controls is the overnight lending rate and the aggressiveness of rate increases thus far in 2022 is unprecedented, as shown in the figure below.

The steepness of this cycle’s rate hikes, and the Federal Reserve’s renewed commitment to maintain this trajectory, have rattled markets and caused many to question if the Fed is moving too fast. Inflation has many components, but one is an imbalance between supply and demand. The Federal Reserve cannot affect the supply side of the markets for goods and services, but through increasing interest rates, it can have a profound impact on the demand side. Mortgage rates are a true reflection of this impact. At the start of this year, 30-year mortgage rates averaged about 3.0%3, but on the last day of September, the average rate had climbed to 6.7%. As most people purchase a home based on what they can afford on a monthly basis, this surge in financing costs will reduce home affordability and act as a drag on current home prices. There is little doubt that the Fed’s actions will eventually work to slow down inflationary forces, but the big question is at what cost? As Chair Powell admitted, this process might “bring some pain,” but the question is how much?

Fixed Income

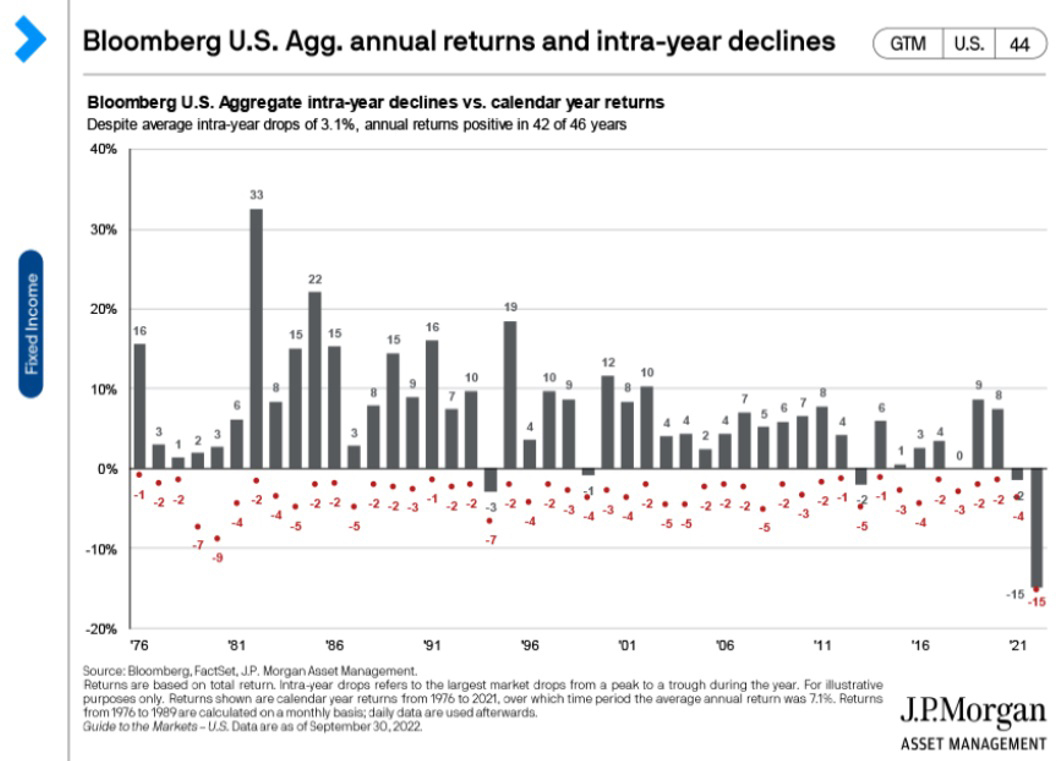

This is the worst drawdown for the bond market in modern history – as the chart below shows, the current 15% decline in the Bloomberg U.S. Aggregate Index is five times the worst annual drop of the last 50 years.

The continued decline of this Index means that bonds have had negative returns for three consecutive quarters. The 30-year Treasury, once considered a safe haven in volatile market environments, has declined by 31.5% in 2022. Investment-grade corporate bonds are down over 18% year-to-date, and even municipal bonds are down 12%.

It may be hard to remember, but at one point in 2019, 40% of world sovereign debt was yielding a negative interest rate.4 In 2020, Germany’s 10-year bond yield was as low as -0.60% and the U.S. 10-year Treasury rate spent a good part of that year under 1%. Investment managers throughout the country were having discussions about how to invest if the negative yields seen around the world spread to the U.S. Instead, the opposite has happened, and the speed of the upturn in rates is unprecedented. At the end of the third quarter, the 5-year Treasury yielded 4.06%, while the 10-year Treasury had climbed to 3.83%. High-yield bonds, representing a debt investment in companies with lower credit ratings, went from yielding about 4.5% at the start of the year to 9.5% at the close of this quarter.

This quarter, Cape Cod 5 has not made any changes to fixed income portfolios, but the changes made in the second quarter definitely proved helpful, as we decreased our allocation to two sectors which continued to underperform – high-yield and emerging market debt. The team’s tactical decision to slightly increase the duration of fixed income portfolios, while emphasizing credit quality, has also been beneficial and should continue to help as the economy braces for a possible recession in 2023.

Equity

Equity markets shook off a significant rally in July, continuing the downtrend started in the first half of the year. All the major averages finished the quarter at a low for 2022, confirming that we are now solidly in a bear market.

The S&P 500 declined an additional 4% for the quarter, bringing total losses for the year to 23.9%. The technology-heavy NASDAQ saw an even greater decline, now down 33% year-to-date. The significant decline in equity markets does mean that valuations have become more attractive. The question is how will corporate earnings fare going forward? Will earnings stabilize or even begin to grow as we enter 2023, or will we see strong revisions downward, making the currently “cheaper” market appear more reasonable or even overvalued? The upcoming earnings announcements, especially the guidance companies give on their prospects for 2023, will be carefully dissected by market observers.

Markets are experiencing one big change now that could provide a headwind towards any sustained market rally in the near term: the death of TINA. TINA is an acronym for “there is no alternative” and refers to investors forced to take on risk, which exceeds their comfort level, to get a fair return. In a long era of low to zero interest rates, investors who might normally buy relatively risk-free CDs or park their funds in money markets started looking at riskier fixed income or equity offerings. Such investors were always wary of their positions and the markets in 2022 have reminded them why. Now, with 2 to 5 year Treasuries offering around 4%, less risky options are appealing. More measured equity investment may ensue as investors make this choice, with sidelined cash migrating to more attractive fixed income returns.

Economy

In our last market update, we opined that the warning lights of a recession were flashing yellow. While the lights are not red yet, many leading indicators are signaling a much higher likelihood of recession coming soon. Since early this year the stock market has been pricing in what is at least a significant slowdown. The latest ISM manufacturing index numbers for September came in surprisingly lower than forecasted, showing the slowest growth in factory orders since early 2020. The Conference Board Leading Economic Index® (LEI) decreased again in August and has fallen 2.7% over the last six months, strongly suggesting an imminent recession.

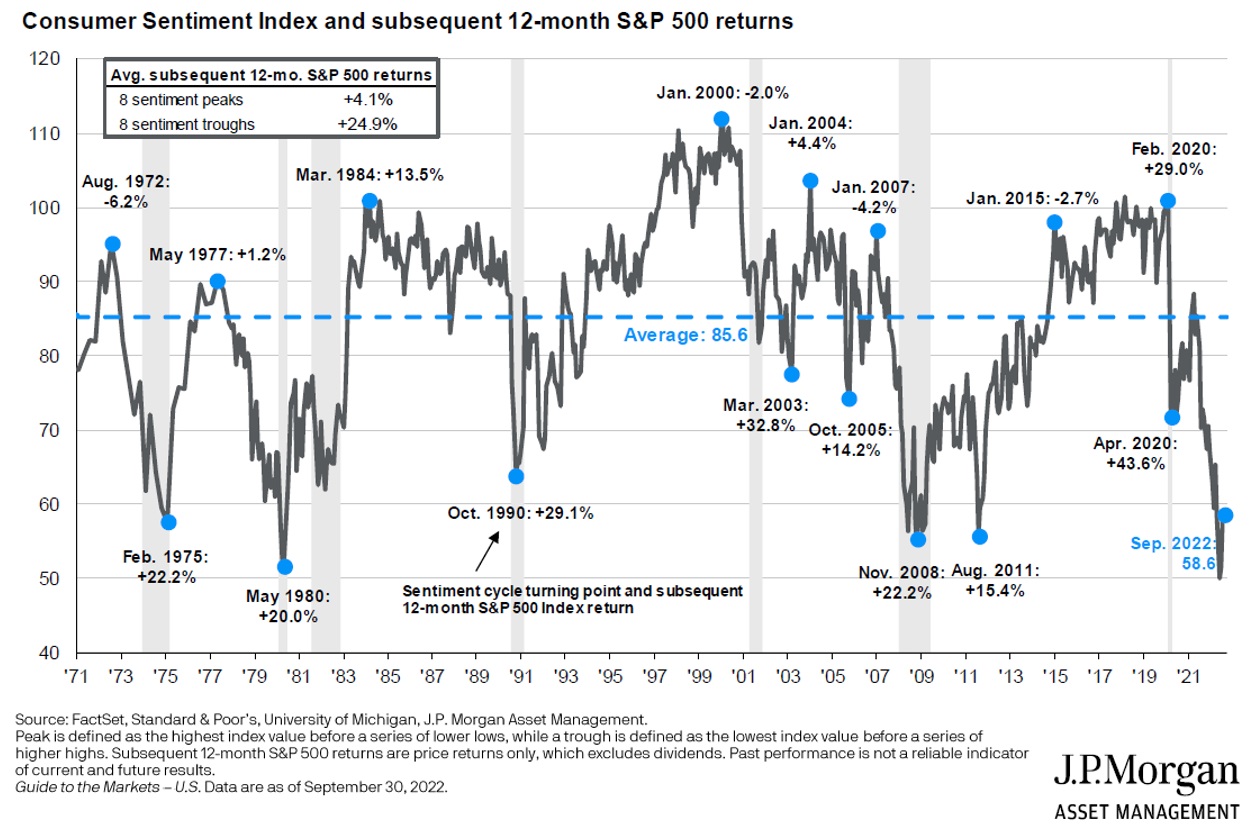

What has made economic predictions so difficult is the continued strength of both the U.S. consumer and the labor market. Since our economy relies so heavily on consumer spending, consumer sentiment warrants monitoring. The University of Michigan runs a survey that builds a Consumer Sentiment Index (UMCSENT); this summer it hit an all-time low of 50 versus a long-term average of 85.6. This change confirms what the stock market signals, but the latest reading in September was 58.6, still historically low, yet still a noticeable uptick from this summer.

The labor market is proving to be most resilient as the economy slows down. The unemployment rate has averaged 6.2% over the last 50 years and now still sits under 4%. Job openings are still at historically high levels and wage growth is fairly strong. The jobs report provides real hope that if there is a recession soon, it will most likely be fairly mild.

Conclusion

For many investors, 2022 has been the most challenging year they have ever seen, with rare multi-quarter declines across both stocks and bonds. To put it in historical context, during the Great Financial Crisis in 2008, the classic 60% equity/40% fixed income portfolio allocation was down 21%. Year-to-date 2022, the same 60/40 portfolio, using the S&P 500 for equity returns and the Bloomberg U.S. Aggregate for fixed income, is down 20%. During the last nine months, at Cape Cod 5, our clients have benefitted from our portfolio construction, bond portfolio duration and stock selection decisions and have meaningfully better relative performance than the benchmark 60/40 portfolio returns cited above.

Coming into the final quarter of 2022, there is far more optimism about future long-term equity and fixed income returns. Stocks have already priced in a slowdown and if inflation appears under control, the Federal Reserve could slow down the rate and duration of future interest rate hikes. Any indication from the Fed that it might be less aggressive could send stocks sharply higher. On the bond side, interest rates are much higher now and investors are enjoying yields that they haven’t seen in fifteen years.

We know that this year has been difficult and on the last day of September, the stock market fell to a new low for 2022. While investor sentiment is weak, it is again important to look at what history has shown us. The chart below shows other times in the last 50 years when investor sentiment has been this low. If you look at the box on the upper left, you will see what has happened, on average, over the twelve months following the low point: the market has returned almost 25%! There is no guarantee that 2023 will be this good, but the past has shown that, when everyone dislikes the stock market, it’s often a good time to invest.

At Cape Cod 5, we believe strongly in our investment process and always seek opportunities to position our portfolios, not only for the current environment, but for an often uncertain future. Meeting clients’ goals and objectives is best achieved through discussion to insure that investment allocations are based on risk tolerances, time horizons, and unique needs and circumstances.

Thank you for placing your confidence in Cape Cod 5. It is a privilege to be your trusted financial advisor.

Jonathan J. Kelly, CFP®, CPA

Senior Investment Officer

On behalf of Cape Cod 5 Trust and Asset Management Investment Committee

Michael S. Kiceluk, CFA, Chief Investment Officer

Brad C. Francis, CFA, Director of Research

Rachael Aiken, CFP®, Senior Investment Officer

Jonathan J. Kelly, CFP®, CPA, Senior Investment Officer

Benjamin M. Wigren, Senior Investment Officer

Kimberly Williams, Senior Wealth Management Officer

Robert D. Umbro, Senior Investment Officer

Craig J. Oliveira, Investment Officer

Alecia N. Wright, Investment Analyst

1 Washington Post 8/26/2022 https://www.washingtonpost.com/business/2022/08/26/fed-powell-jackson-hole/

2 U.S. Bureau of Labor Statistics https://www.bls.gov/opub/ted/2022/consumer-prices-up-9-1-percent-over-the-year-ended-june-2022-largest-increase-in-40-years.htm

3 FRED economic data https://fred.stlouisfed.org/series/MORTGAGE30US

4 MarketWatch 3/25/2022 https://www.marketwatch.com/story/global-pile-of-debt-at-negative-yields-dips-below-3-trillion-deutsche-bank-11648237773

These facts and opinions are provided by the Cape Cod 5 Trust and Asset Management Department. The information presented has been compiled from sources believed to be reliable and accurate, but we do not warrant its accuracy or completeness and will not be liable for any loss or damage caused by reliance thereon. Investments are NOT A DEPOSIT, NOT FDIC INSURED, NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY, NOT GUARANTEED BY THE FINANCIAL INSTITUTION AND MAY GO DOWN IN VALUE.

Read recent Market Reviews

Market Review Q2 2022 | Market Review Q1 2022 | Market Review Q4 2021 | Market Review Q3 2021

Market Review Q2 2021 | Market Review Q1 2021

Contact our Wealth Team More Market Insights from Cape Cod 5